What Is Maharashtra’s Self-Redevelopment Scheme for Housing Societies and Why It Needs a Financial Lifeline

In September this year, the Reserve Bank of India (RBI) refused permission to Maharashtra’s state and district central co-operative banks (DCCBs) to finance self-redevelopment of co-operative housing societies, stating that such projects would fall under the category of ‘commercial real estate,’ and hence, outside the banks’ primary purview of lending for activities related to agriculture and rural development. For the Maharashtra government, which was banking on support from the state’s co-operative banking ecosystem, this is as a huge blow to a scheme it had presented late last year as the solution to the state’s, and more specifically, Mumbai’s housing crisis. Meanwhile, with over Rs. 1,350 crores sanctioned and another Rs. 17 crores disbursed in loans for such projects, RBI’s decision leaves the Mumbai District Central Cooperative Bank (MDCCB) and several housing societies with an uncertain way ahead.

While Mumbai grew spectacularly as an urban centre in the years following India’s independence, the geographical constraints of the island city have caused serious problems today; with a premium attached to limited land and space, real estate prices have skyrocketed. Apartments in newly constructed buildings and housing societies, a product of urban development driven by builders, are unaffordable to most of the city’s population. For instance, for a middle class family with an average annual income between Rs. 5,00,000 and 7,00,000, buying a 600-square-feet apartment that would cost about Rs. 2.1 crores - almost thirty times their average annual income - is nearly impossible. On the other hand, a considerable percentage of the city’s existing housing stock lies dilapidated and offers unsafe and poor living conditions. According to data from the Maharashtra Housing and Area Development Authority (MHADA), 14,000 buildings in the city are in dire need of remediation, with 25,000 to 30,000 housing societies having expressed a desired interest in redevelopment.

Redevelopment, however, isn’t a novel concept and has been promoted by successive governments over the past few decades. Traditionally, a housing society would enter into an agreement with a developer, who would be liable to hand over the apartments to their respective owners upon construction with pre-established benefits such as a 10 percent increase in area or a given amount of corpus money. To achieve this, the developer would utilize the balance plot potential by constructing and selling additional apartments and shops as per approval from statutory bodies. This was and continues to be a lucrative venture for developers - working without oversight and at their own discretion, developers can sell the additional real estate at exorbitant prices and earn huge profits. However, housing societies and residents would often be left with poorly designed and/or constructed buildings, subjected to inordinate delays, and sometimes, even the abandonment of the project by the developer. Consequently, a framework for the regulation of such power was put in place under the RERA (Real Estate Regulatory Authority) so developers couldn’t divert funds from one project to another and thus, increase risk. But that wasn’t enough - a new and better model of redevelopment was needed.

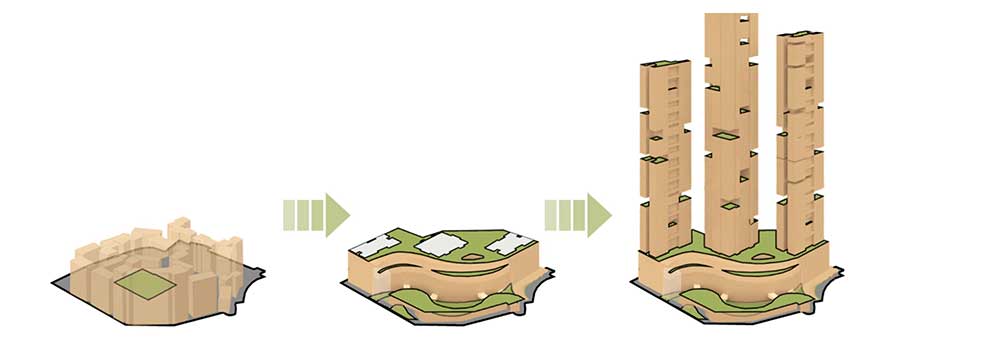

In September 2019, the Maharashtra government introduced the self-redevelopment scheme for co-operative housing societies with a Government Resolution (GR). The aim: empowering residents to take control of the redevelopment process through its entire timeline - from commissioning a suitable architectural or contracting firm and managing construction to selling the additional real estate constructed and sharing the final profits. The autonomy of the process guarantees merit in all respects; society members would reap the benefits of good quality construction, modern amenities and infrastructure, and time-bound and cost-controlled construction. Additionally, with the developer removed from the process, there would be no risk of fraud, delayed construction, or loss of area; in fact, residents could expect up to 40-50 percent increase in carpet area compared to 15-20 percent through the traditional process. Most importantly, however, self-redevelopment would bring down the cost of the surplus apartments built (as opposed to the price inflation that occurs when a developer who is driven by profit margins is involved) creating a ripple effect in the market and ensuring housing remains affordable to the masses.

To promote the scheme, the government said that it would offer 10 percent additional FSI (Floor Space Index) over the permissible figure, concessions in TDR (Transfer of Development Rights) and other construction premiums to housing societies opting for self-redevelopment. Additionally, the Maharashtra State Co-operative Bank (MSCB) was appointed as the nodal bank to work through the district central co-operative banks (DCCBs) to provide loans to societies at relatively lower interest rates of around 12.5 percent as opposed to around 18 percent offered to developers. With the RBI’s recent notification, this critical link has been severed - without financial support for self-redevelopment, housing societies will have no choice but to go back to the vicious builder-driven model of redevelopment. There is an urgent need to bridge this gap.

The decision from RBI has some pretty obvious loopholes and deserves questioning. What happens, for instance, if a district co-operative bank serves a completely urbanised area? The MDCCB is the perfect example; local housing societies own a majority stake in the bank, and its area of operations, which extends from Colaba and CST in southern Mumbai to the neighbourhoods of Dahisar and Mulund at the city’s northern periphery, doesn’t house any farmers or agricultural land. The MSCB, therefore, must immediately file an appeal with the central banking regulator to reconsider and/or clarify its decision publicly. Meanwhile, private investment firms and financial institutions must come in and participate too; self-redevelopment can yield returns on investment (ROI) of as much as 12 percent. This transparent and democratic model that enables people to carve their own sustainable future needs to be safeguarded if we are to solve Mumbai’s housing crisis.